Kindly open the website on a laptop or desktop, as the mobile version is currently under construction.

Why Small-Cap Exposure Matters: Lessons from Custom Index Construction

We built custom equity indexes using three different weighting schemes and discovered that broader market exposure significantly outperformed large-cap benchmarks like SPY and QQQ over 20 years. Built with Python, WRDS, CRSP data, and Jupyter for reproducible financial analysis.

Mohar Chaudhuri, Melissa Cai Shi, Cassandre Korvink-Kucinski

1/24/20263 min read

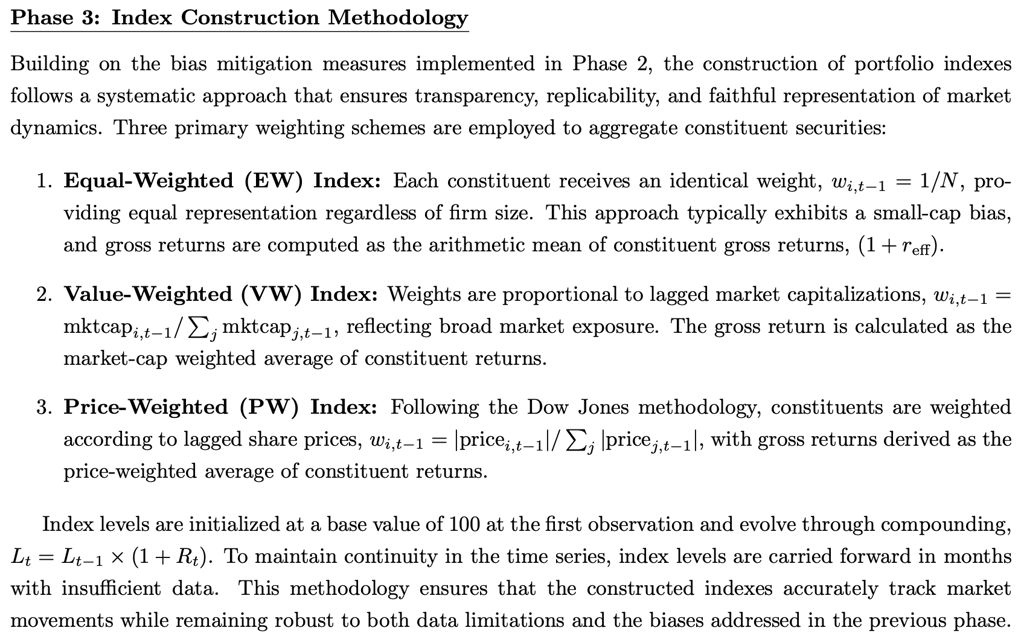

Methadology Overview

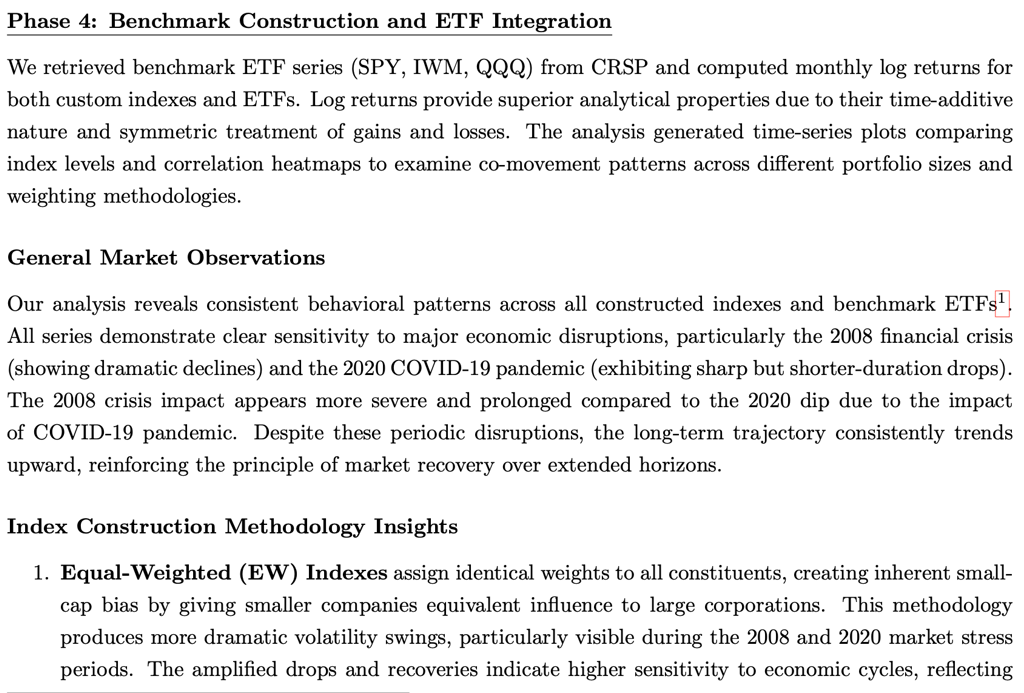

Portfolio Size Analysis and Benchmark Comparisons

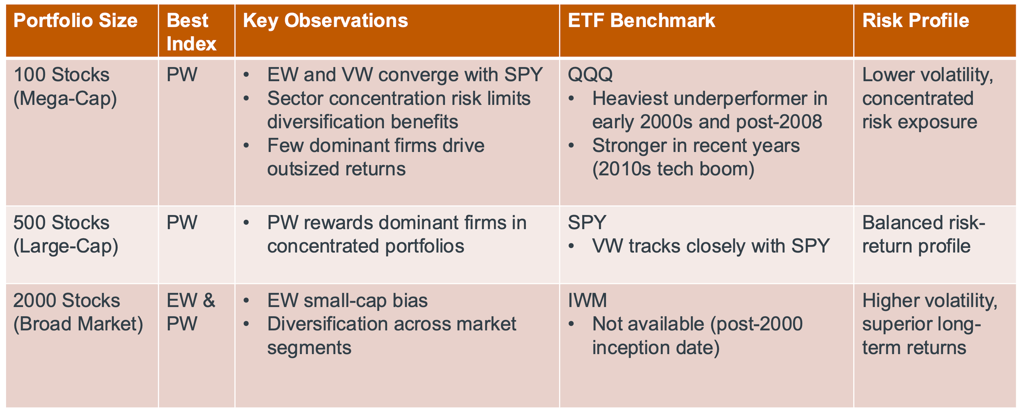

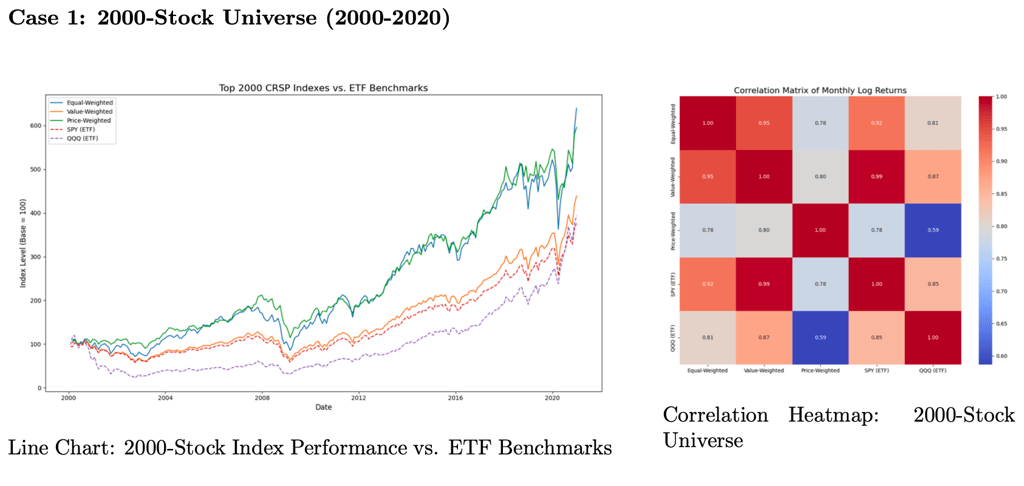

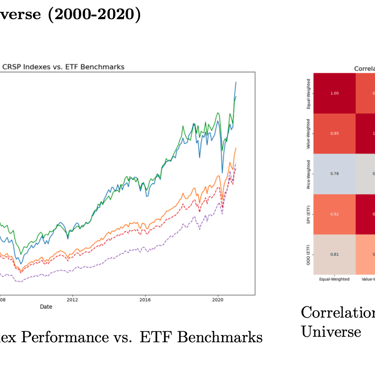

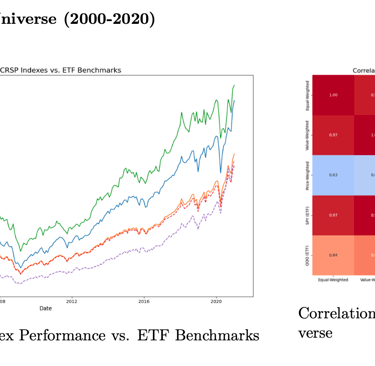

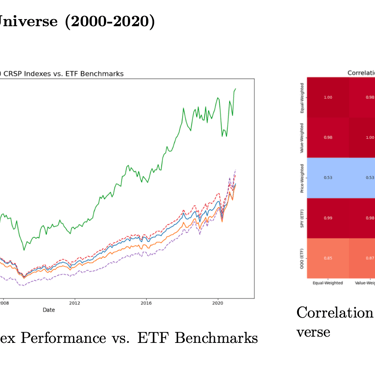

We constructed custom equity indexes across three weighting methodologies (equal-weighted, value-weighted, and price-weighted) using CRSP data from 2000-2020 and benchmarked them against major ETFs. The equal-weighted and price-weighted indexes tracking 2000 stocks dramatically outperformed SPY (~500% vs. 250% cumulative return) and QQQ, primarily due to broader market exposure capturing the small and mid-cap premium. In contrast, the value-weighted index tracked closely with SPY due to large-cap concentration, while QQQ lagged significantly from its heavy tech sector exposure. This analysis demonstrates that broader diversification across market capitalizations—rather than concentration in large-cap or sector-specific stocks—delivers superior risk-adjusted returns over extended periods.

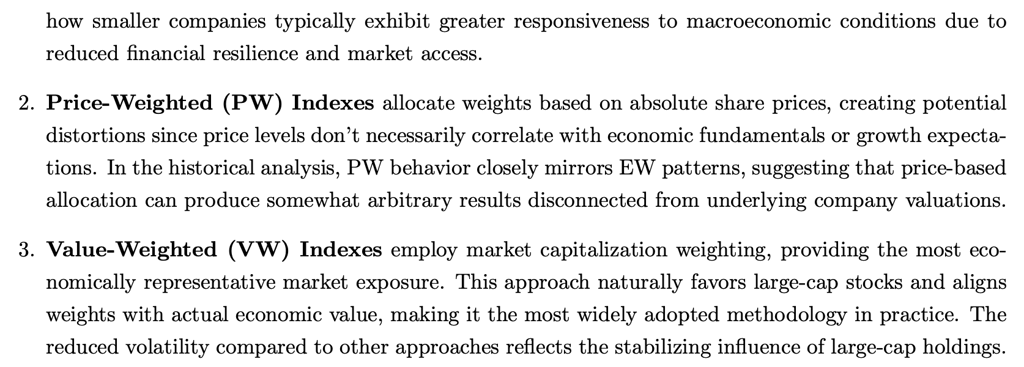

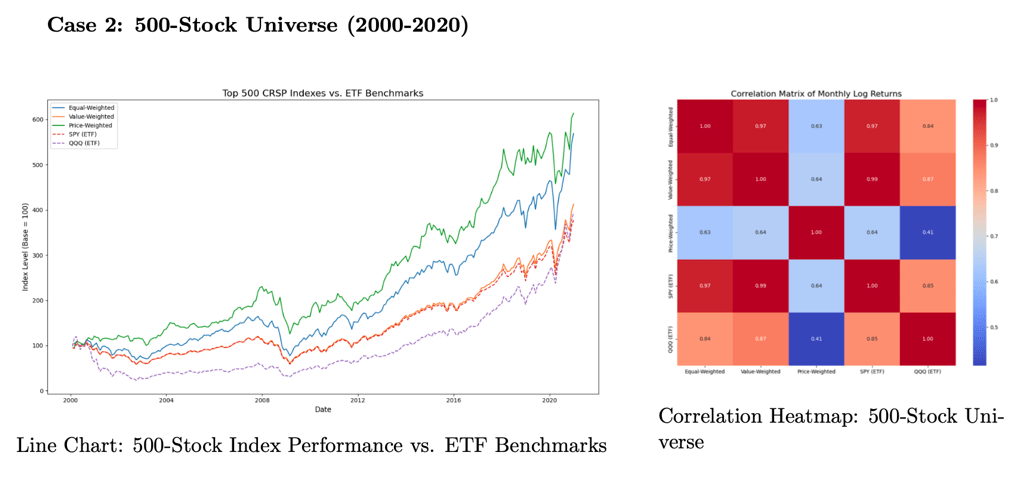

In the 500-stock universe, the price-weighted index emerged as the strongest performer (~560% cumulative return), outpacing both equal-weighted (~440%) and value-weighted (~300%) indexes, as well as SPY and QQQ. This shift from the 2000-stock results reflects increased large-cap concentration—the price-weighted approach gave more weight to high-priced dominant firms (often tech leaders), which drove superior returns in this subset. The value-weighted index closely tracked SPY due to shared large-cap exposure, while equal-weighting's outperformance diminished compared to the broader 2000-stock universe since there were fewer small/mid-cap stocks to capture premium returns. QQQ lagged in early years but showed relative strength post-2010 as large-cap tech stocks dominated, highlighting how concentration in a narrower universe fundamentally changes the effectiveness of different weighting methodologies.

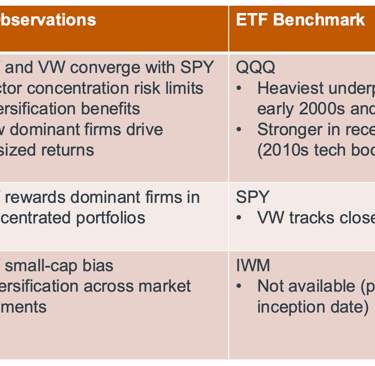

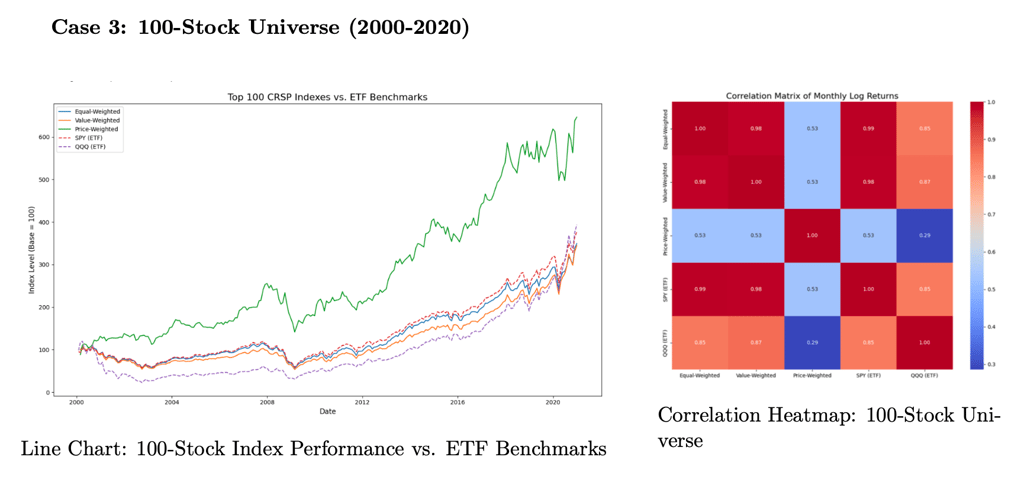

In the most concentrated 100-stock universe, the price-weighted index dramatically outperformed all other methodologies (~620% cumulative return), more than doubling the equal-weighted (~280%), value-weighted (~260%), and SPY (~250%) returns. This stark divergence reveals how a handful of high-priced mega-cap firms—predominantly tech stocks—dominated performance when the universe is this narrow. Notably, equal-weighted and value-weighted indexes converged and tracked closely with SPY, demonstrating that diversification benefits essentially disappear in highly concentrated large-cap portfolios where there's no small/mid-cap exposure to capture premium returns. QQQ performed similarly to SPY in recent years due to substantial overlap with the top 100 stocks, while the price-weighted index's dominance underscores the extraordinary impact of a few leading firms during the 2010s tech-driven bull market.

Our analysis reveals a striking pattern: the broader your exposure, the better your returns. The 2000-stock equal-weighted index crushed benchmarks with 500% gains by capturing the small-cap premium that SPY and QQQ completely miss. As we narrowed to 500 stocks, the advantage shifted to price-weighting as mega-cap winners took control. By the time we hit the top 100 stocks, diversification died—equal, value, and market-cap weighting all converged around 250-280% returns, while only price-weighting's bet on a few high-priced giants delivered outsized gains. The takeaway? In investing, casting a wider net catches bigger fish. Wall Street's obsession with large-cap concentration leaves billions in small and mid-cap returns on the table.

Connect with me!

© 2025. All rights reserved.

Whether you're a seasoned data scientist, a fellow learner on this journey, or someone curious about what data can reveal, I'd be delighted to connect. Please drop me a message.