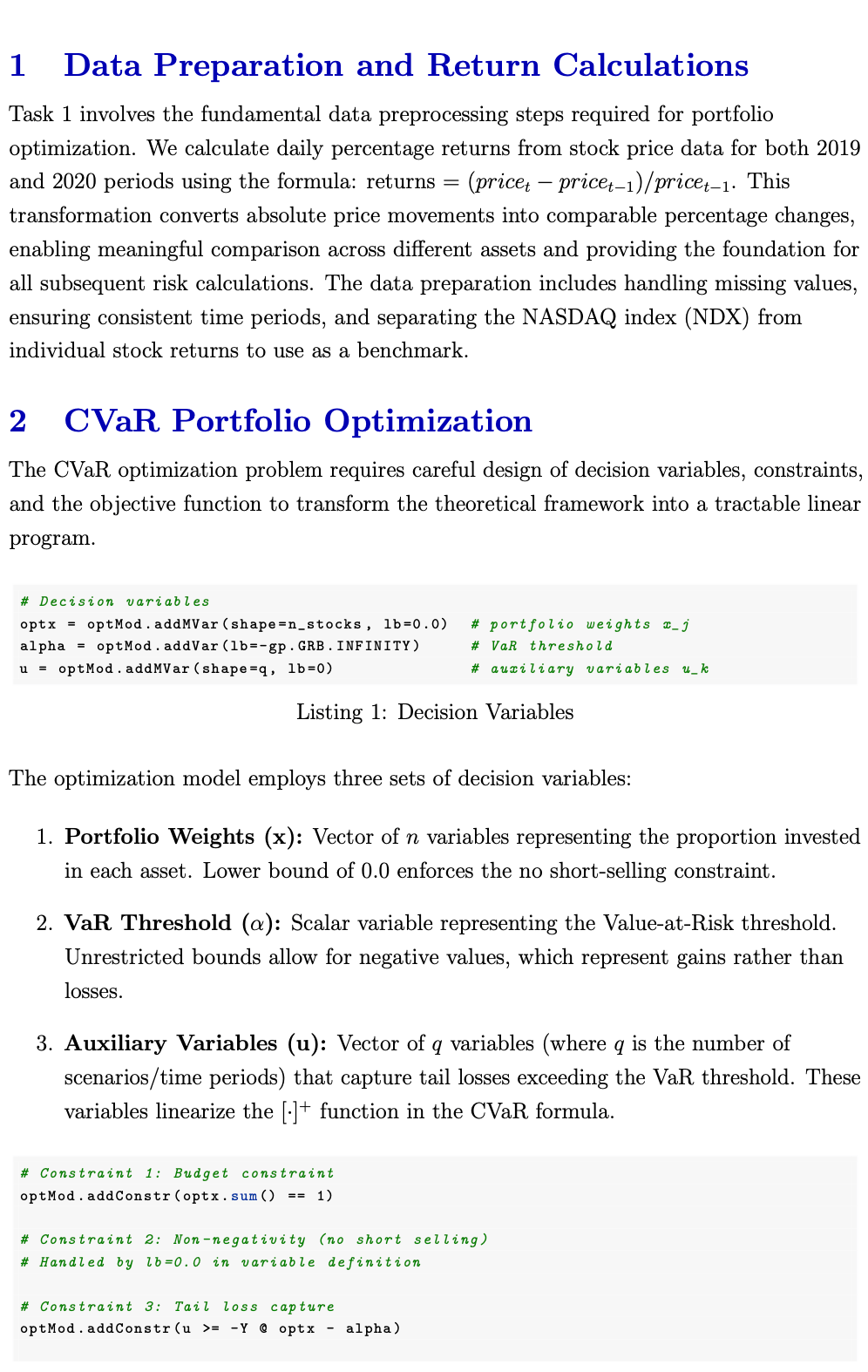

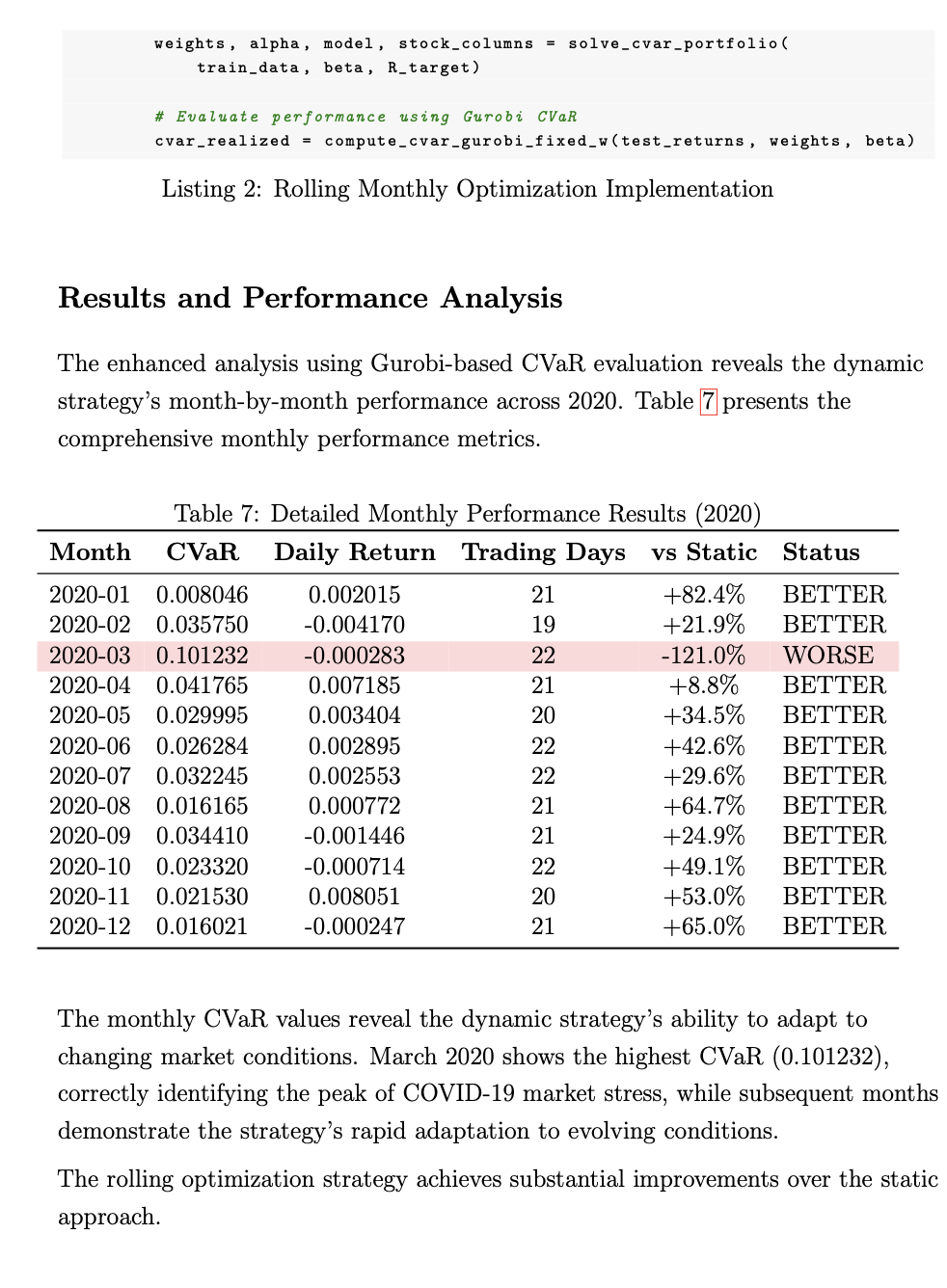

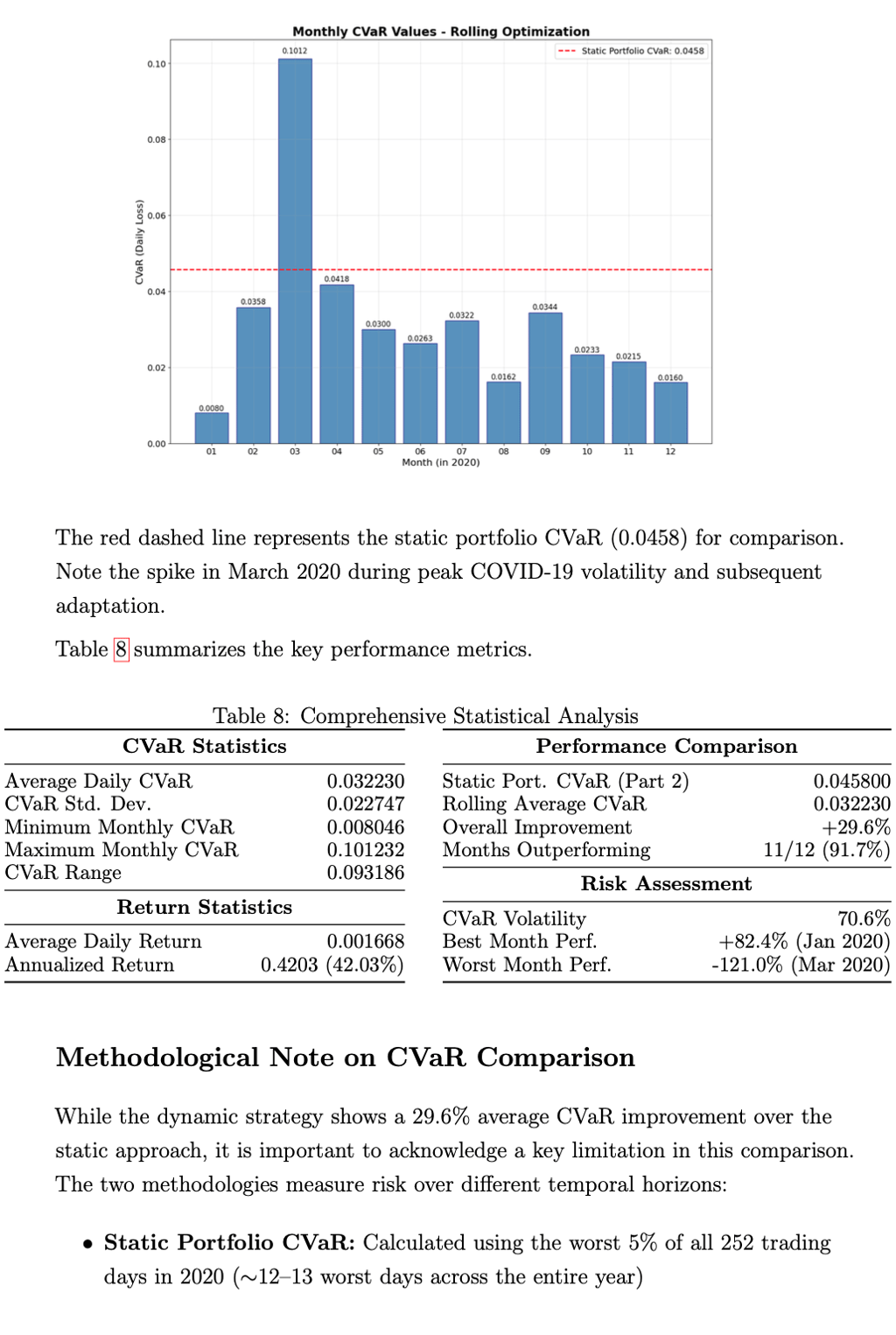

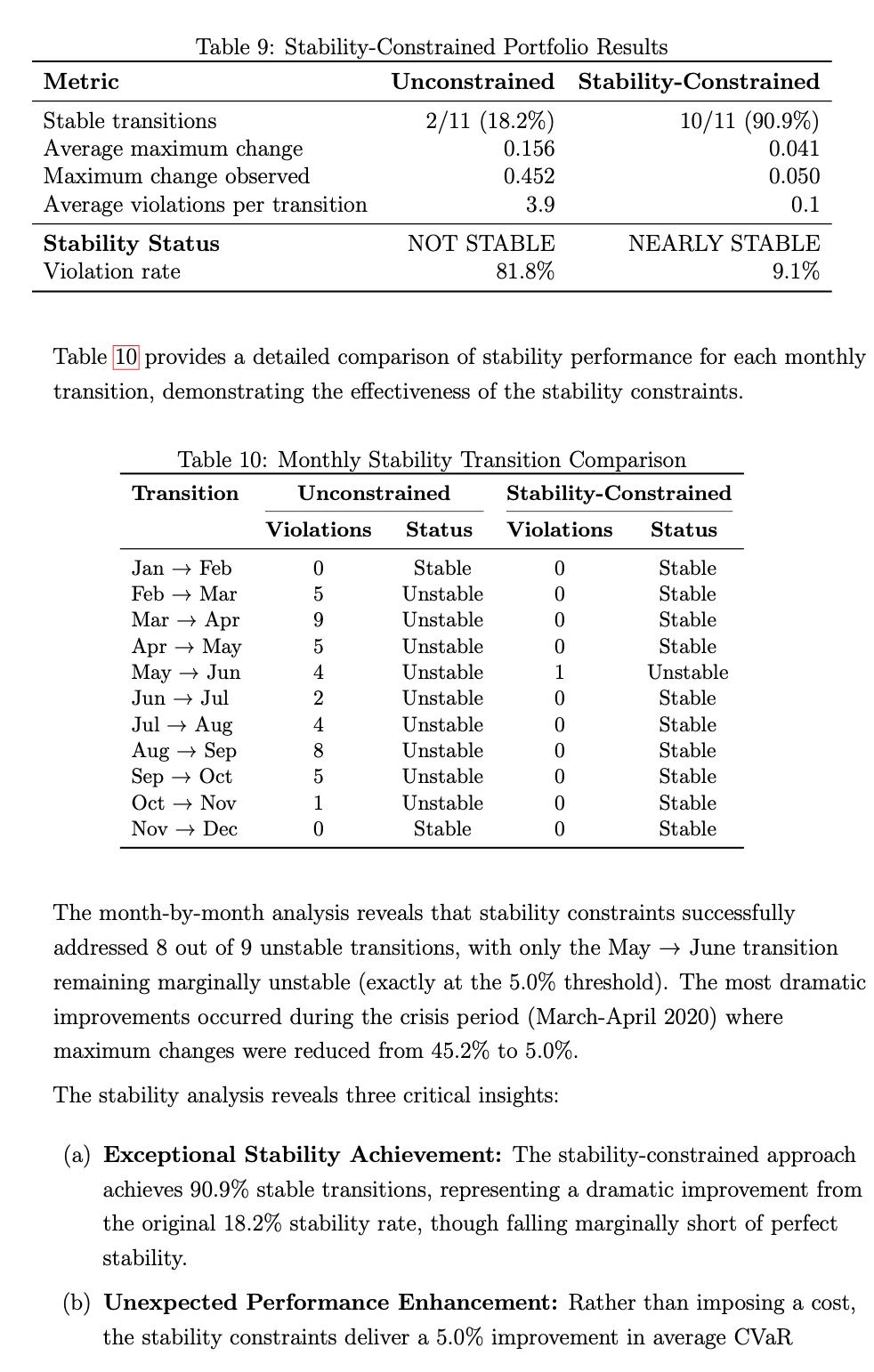

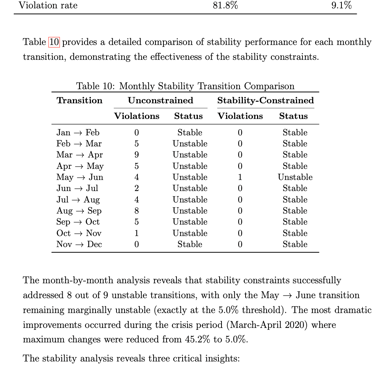

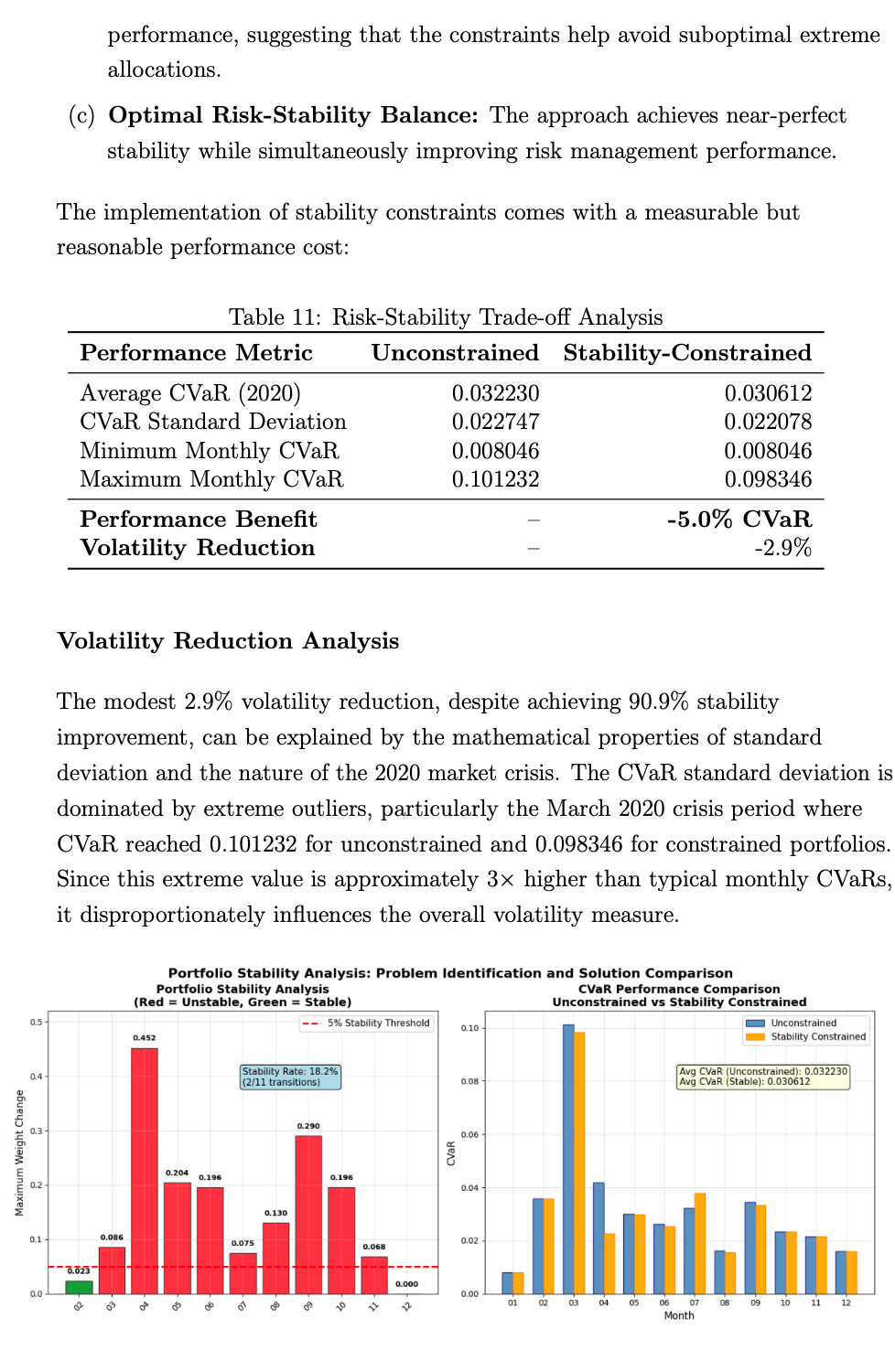

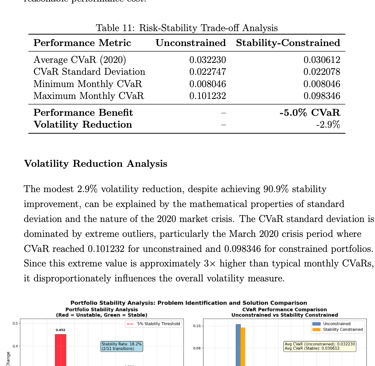

CVaR Portfolio Optimization

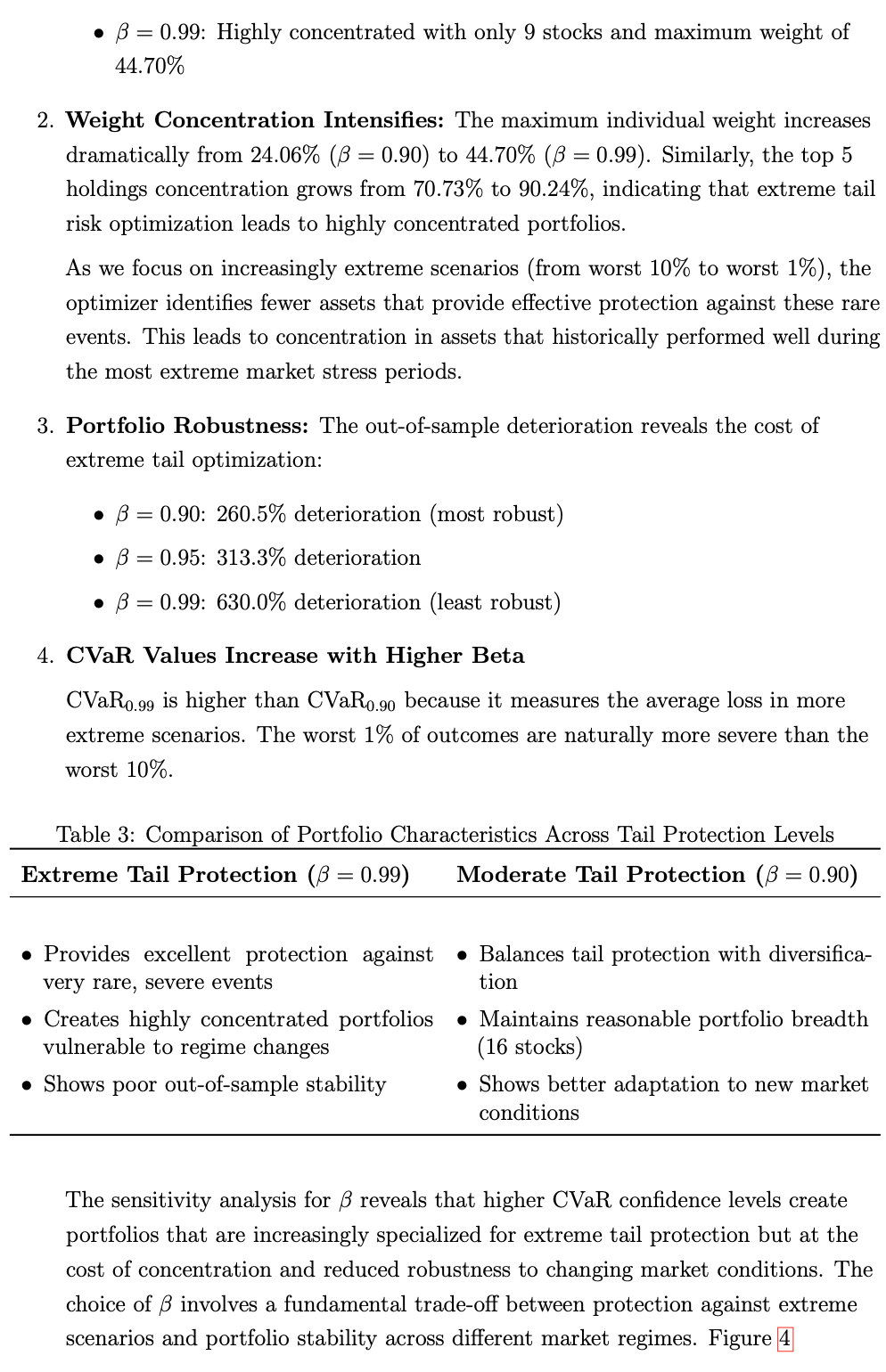

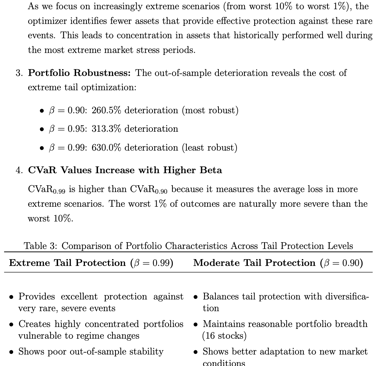

This study examines five portfolio optimization strategies using Conditional Value-at-Risk (CVaR) minimization across different market conditions. We analyze standard CVaR optimization, sensitivity across confidence levels, minimax approaches, dynamic monthly rebalancing, and stability-constrained implementations. Stability constraints successfully maintain most risk bene- fits while enforcing practical implementation limits. The findings demonstrate that CVaR frameworks can effectively adapt to different objectives, from average performance to extreme tail protection, with distinct risk-return- stability trade-offs for varying investor preferences.